August Feeders Down $3.525; Boxed Beef Down $6.09 In 2 Days

Negotiated cash cattle trade was active on good demand in Kansas on Thursday, with live purchases reported at $255/cwt, steady with Wednesday. Trade in Nebraska and the Western Corn Belt was lighter with moderate demand. In Nebraska, live sales were reported at $255/cwt, $1 lower than Wednesday, while a few dressed sales were reported at $403/cwt, though volume was too light to establish a market. The previous dressed market in Nebraska was mostly $403/cwt on Wednesday. In the Western Corn Belt, live purchases ranged from steady to $1 lower at $255/cwt compared to Wednesday, while the last established dressed market was $403/cwt. No new trade was reported in the Texas Panhandle, where the last established market was $258/cwt on a live basis last week.

Cattle futures closed lower on Thursday. August live cattle settled at $239.225/cwt, down $2.60, while August feeder cattle finished at $360.625/cwt, down $3.525. In the grain markets, July corn closed at $4.25/bu, up 4 cents. Outside markets were mixed. August crude oil settled at $68.48 per barrel, down $0.10, while the Dow Jones Industrial Average gained 594.83 points to close at 52,900.07.Boxed beef values declined for the second consecutive session on Thursday. The Choice cutout fell $4.19 to $387.07, while the Select cutout declined $2.26 to $367.43. The Choice/Select spread narrowed to $19.64, down from $21.57 on Wednesday, with movement totaling 112 loads, one fewer than the previous day. Over the past two trading sessions, the Choice cutout has fallen $6.09. Compared to Wednesday, primal values were mostly lower. The rib eased $0.31 to $581.89, the round declined $9.38 to $324.55, the loin dropped $8.57 to $486.16, the brisket slipped $1.43 to $342.38, the plate fell $9.92 to $286.78, and the flank declined $1.32 to $245.78. The chuck was the only primal to post an increase, gaining $1.96 to $335.56.

Federally inspected cattle slaughter totaled 109,000 head on Thursday, unchanged from the previous Thursday but 4,703 head below the same day last year. Week-to-date cattle slaughter stands at 433,000 head, matching the pace of the previous week but trailing 472,421 head processed during the same week a year ago. Year-to-date federally inspected cattle slaughter totals 13.745 million head, down 8.7% from 15.050 million head during the same period in 2025.

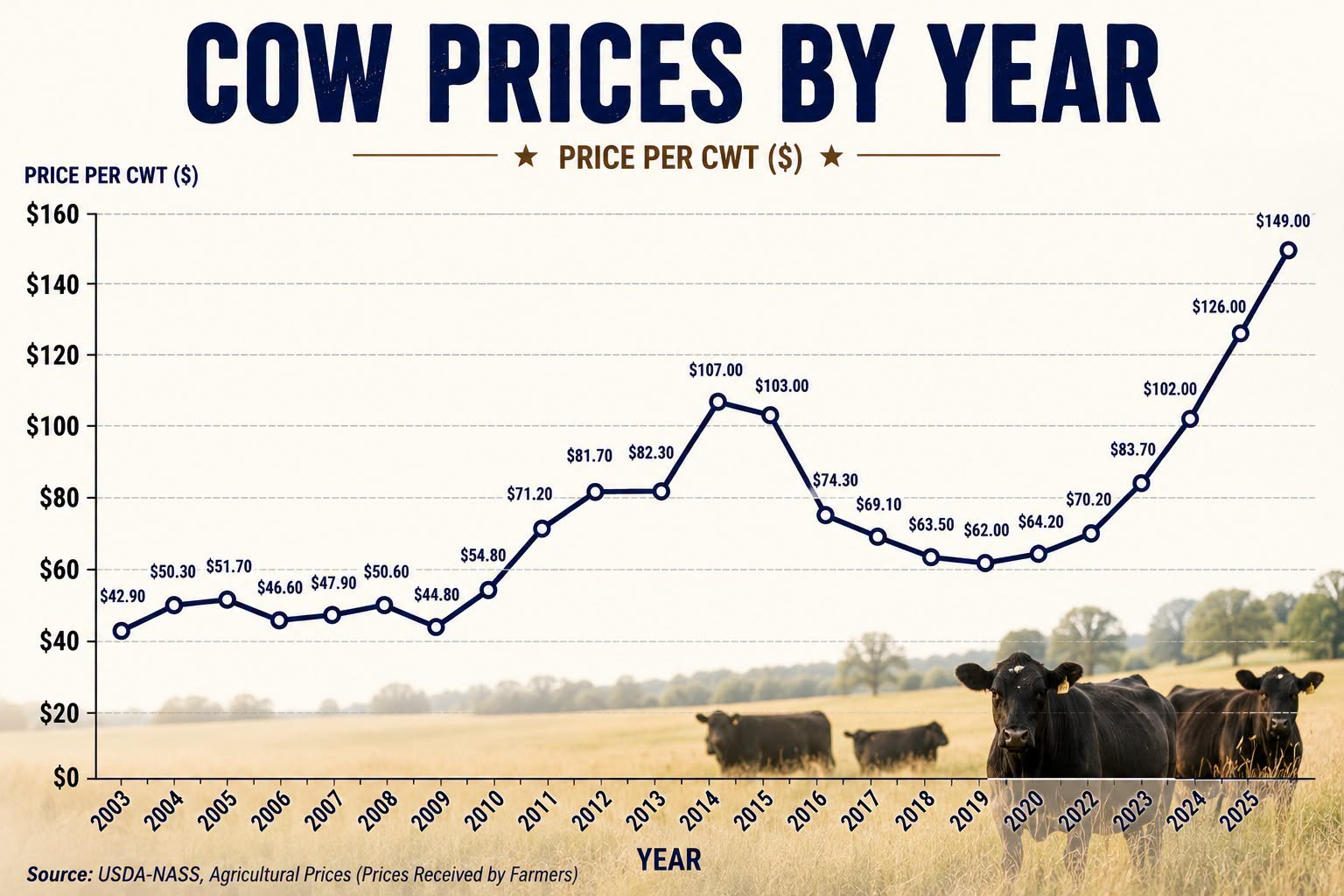

2025 U.S. Cow Prices Set Record High, Up 247% Since 2003

Annual cow prices in 2025 averaged a record $149.00/cwt, the highest annual average ever recorded in the United States. That was $23.00/cwt, or 18.3%, higher than the $126.00/cwt average in 2024. The rally has been even more dramatic over the longer term, with cow prices climbing 140.3% since 2019, when they averaged just $62.00/cwt. Prior to the current market, the previous cycle high was $107.00/cwt in 2014, meaning 2025 prices are 39.3% higher than that peak. Looking back even further, annual cow prices have surged from $42.90/cwt in 2003 to $149.00/cwt in 2025, an increase of 247.3% over the past 22 years, highlighting the historic strength of today's cow market.

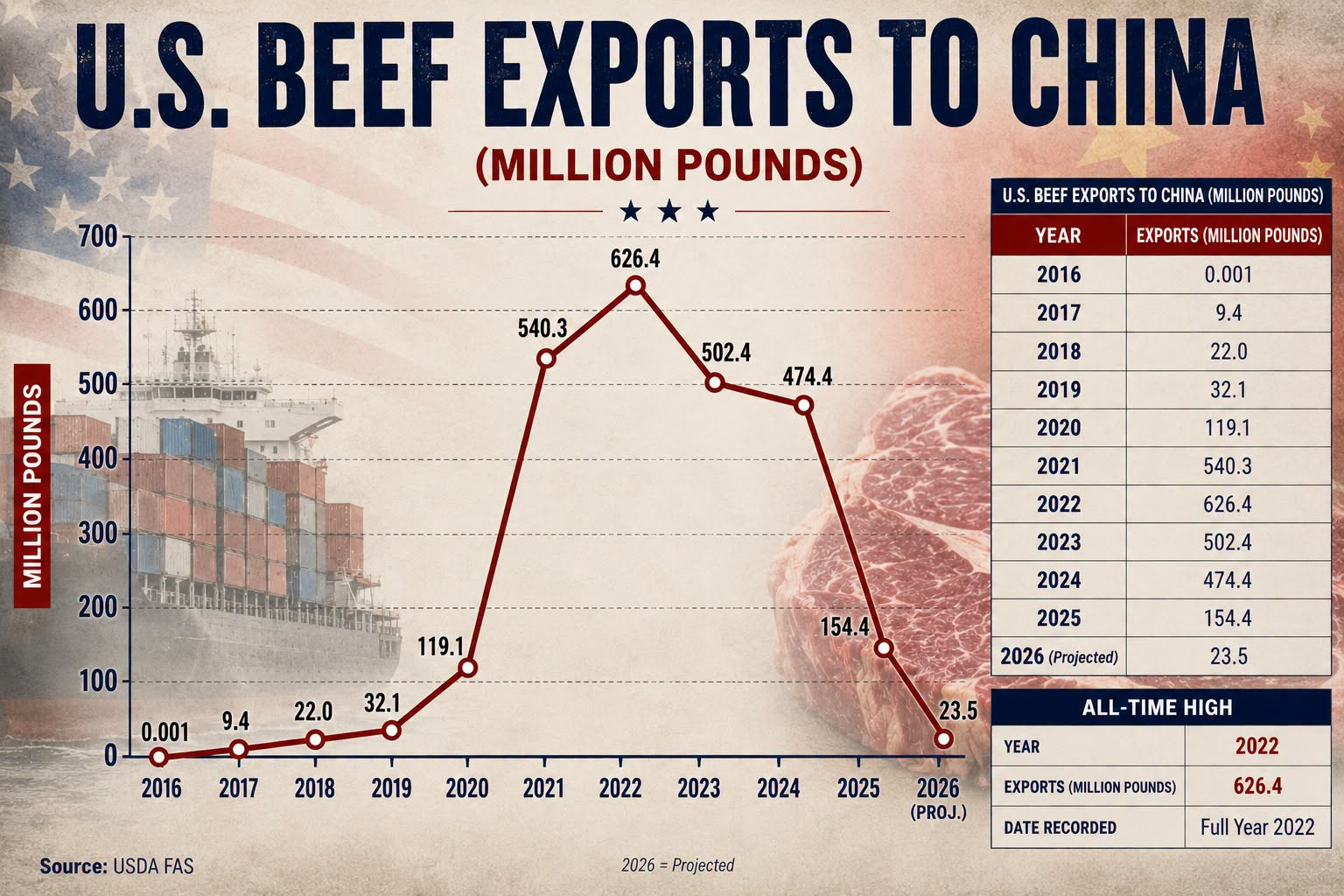

U.S. Beef Exports to China Projected to Fall Back Near 2019 Levels

U.S. beef exports to China totaled 154.4 million pounds in 2025, down sharply from 474.4 million pounds in 2024. Exports are projected to fall even further in 2026 to just 23.5 million pounds, with only 6.2 million pounds shipped through April.

After remaining virtually nonexistent prior to 2020, exports surged from 119.1 million pounds in 2020 to a record 626.4 million pounds in 2022 before beginning a steep decline. If the current projection holds, U.S. beef exports to China will fall back to levels not seen since 2019, marking a dramatic reversal from the record shipments seen just a few years ago.